Two thought provoking days, and a crash course in carbon trading (and carbon trading politics), leaves me with a few key comments (and many more questions). There’s lots of devil in the detail in the documents (which are many, and often thick) – but these are my headlines.

Two thought provoking days, and a crash course in carbon trading (and carbon trading politics), leaves me with a few key comments (and many more questions). There’s lots of devil in the detail in the documents (which are many, and often thick) – but these are my headlines.

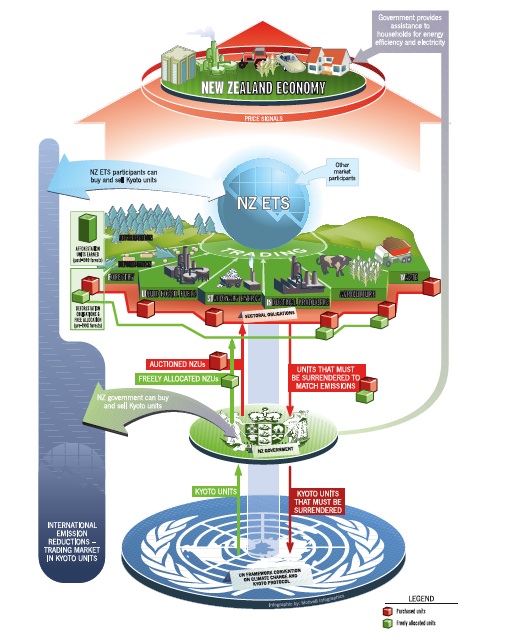

• AGRICULTURE: The next year is going to be a busy one for all sectors, because officials are aiming to give advice to ministers by the end of 2008. The various panels and expert groups are going to be working at a brisk pace. Key questions are around the “€œpoint of obligation” – the point where the carbon has to be accounted. The “€œbest” way would be at farm level, so that farmers get a direct signal about the carbon content of their decisions, and can respond, but there are around 35,000 farms – a logistical nightmare. The preference is to operate the ETS at Fonterra or meat processor level. Simpler, but perhaps not so efficient. The five year delay was justified by the need to undertake pilot schemes for emissions monitoring and to conduct more research, but the unavoidable conclusion is that the hard decisions are delayed until after the next election. Necessary and convenient.

* ECONOMIC IMPACTS: All the Treasury modelling shows relatively minor impacts on the economy – from 0.1% of GDP over the five years to 0.24% in a worst case. More modelling will be released soon, but it is expected to show much the same thing. We were shown impacts based on a carbon price of $25/tonne as well as the $15/t used at the launch. This might push costs for the average household up to $330 per year, adding 6.1c to petrol, 6.7c to diesel, 10% to domestic electricity and 18% to wholesale, 18% to gas prices, and a whopping 67% to coal. Of course, it all depends on the market price for carbon – which I’ll discuss later. Although the impact might be low over the whole economy, there will be winners and losers – and some stress for companies that are exposed to international competition. If a big company chose to move out of NZ, for instance, the economic impact might be bigger than the economic modelling suggests, and regional impacts could be important.

• ASSISTANCE: During 2008-12, the first Kyoto commitment period (aka CP1), the government will be supplying many sectors with “assistanceâ€? in the form of free allocations of carbon credits. This is designed to cushion the blow of carbon costs on businesses that can’t immediately pass the cost on to their customers. Liquid fossil fuels, for instance, get no free credits because they’re expected to pass the extra costs straight through to you an me (but I’ll have an electric car). However, these free credits will be phased out over 2013-25, and several major emitters have already signalled that this could be an issue. One company rep at the meeting said that it would force his firm overseas – but that rather assumes that there will be places without carbon pricing available in that time frame. If post-Kyoto is to be effective, it’ll have to address that cross border “€œleakage” – either through a “€œborder adjustment tax” (mentioned by several commenters) or through special industry arrangements. This cut off period also applies to agriculture and forestry, and I predict that it will be one of the key pressure points in negotiations over the next year.

• COST OF CARBON: I’ve blogged on several occasions about how optimistic I regard the government’s pricing of carbon to be – and how this misrepresents the true cost of our emissions overshoot in CP1. After the workshop, I am a little more relaxed about this issue. It’s tempting to look at the current cost of Kyoto units in the European market and assume that will be the sort of price that applies here, but there are a number of reasons for thinking that may not be true. The first is that our scheme will be exposed to international pricing, and we can go where units are cheapest (the least-cost principle that underlies cap & trade), which at the moment is probably clean development credits coming our of China (they have a current floor price of E8, set by the Chinese government to prevent sales at lower prices). $15/tonne remains too low, and $25/tonne may still be on the low side, but even at $50/tonne the total cost over CP1 – if the government’s projections of a 25mT deficit (5mT per year) come true – is about $200m per year. On GDP of about $160 billion (rising to $200b in 2012) that’s about 0.12%, in line with the economic modelling. Not something to lose sleep over. In the long term, and beyond CP1, the cost of carbon is likely to rise. The tougher targets that will be required to meet the climate imperatives will ensure (with luck) a steadily shrinking cap. In the early years the entry of lots of new countries, each with their own schemes, will probably keep the market well supplied with credits as low-hanging fruit for carbon reductions are plucked and eaten, but after that the carbon price is pretty much guaranteed to rise. Bad news for big emitters, good news for foresters, and anyone who has invested in low carbon technologies.

• HOW TO MAKE MONEY FROM CARBON TRADING: Become a carbon trader or a carbon trading consultant, a carbon accountant or an adviser (or, perhaps, a carbon commentator 😉 ). This stuff is complicated and detailed. To make rational decisions you need good advice, and that never comes cheap. Not in brain cells, anyway.

Hello Gareth

Congratulations on this excellent work. I have posted on your blog at:

http://snowybramble.blogspot.com/

Please have a look and let me know if there is any issue.

Cheers

Robert

Look’s fine to me, Robert. Many thanks!