In the wake of the Morgan Foundations hard-hitting report “Climate Cheats”, Simon Johnson (aka Mr February) asks if New Zealand Steel received millions of emission units for free under the New Zealand Emissions Trading Scheme industrial allocation provisions and yet still bought millions of the dubious international Russian units (ERUs) to make windfall arbitrage profits.

The Morgan Foundation’s latest report “Climate Cheats” has been sizzling across the various media in the last week. The language of the report is refreshingly non-neutral and unashamedly emotive. It is in equal parts compelling and condemning.

Carbon credit scheme a farce, reported the Herald. Climate change cheating, said Radio New Zealand. Dodgy deals, climate swindle, climate fraudsters, junk carbon scam, said report author Geoff Simmons.

As a consequence, “Climate Cheats” is an easy and engaging read – no mean feat given the topic – that is also thoroughly well-researched. It really is a ‘high integrity’ credit to it’s authors (if you pardon the pun).

In this post I want to look specifically at one particular type of corporate conduct – arbitrage profiteering – covered in “Climate Cheats”.

Geoff Simmons, on page 28, describes arbitrage like this:

“Meanwhile polluters in New Zealand benefited through a collapse in the price of emissions, while some even creamed off profits by exploiting the price difference between different types of carbon credits.”

How does an emitting company make an arbitrage profit in an emissions trading scheme? I think a data-driven worked example might be informative.

I will look at New Zealand Steel because their CEO was recently whining to Radio NZ that the NZ emissions trading scheme review would lead to higher carbon costs which would make the business less viable.

The data. I need to have the following:

- the number of free emission units allocated by the Ministry for the Environment to New Zealand Steel

- the quantity of New Zealand Steel’s greenhouse gas emissions from processing steel from iron sands from the New Zealand’s Greenhouse Gas Inventory 1990–2013

- the number emission units to surrender under the NZETS, I estimate as half of the emissions under the “two-for-one” deal

- and the number of any of Geoff Simmons favourite dodgy Ukrainian or Russian Emission Reduction Units owned by New Zealand Steel, as compiled from the EPA Emission Unit Register.

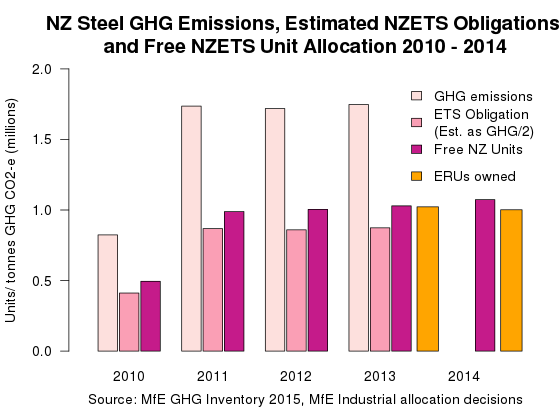

Let me sum that up in a table.

| New Zealand Steel free unit allocation, greenhouse gas emissions and NZETS surrender liability and ERUs | |||||

|---|---|---|---|---|---|

| Year | 2010 | 2011 | 2012 | 2013 | 2014 |

| Units allocated | 494,704 | 989,304 | 1,003,730 | 1,029,352 | 1,073,489 |

| GHG emissions (t) | 1,646,890 | 1,736,250 | 1,718,930 | 1,747,500 | N/a |

| Estimate of units to surrender | 411,722 | 868,125 | 868,125 | 873,750 | N/a |

| Allocation less surrenders | 82,982 | 121,179 | 135,605 | 155,602 | N/a |

| Allocation/Liability (per cent) | 120% | 114% | 116% | 118% | N/a |

| Emission Reduction Units owned at 31 December | N/a | N/a | N/a | 1,022,527 | 1,001,714 |

Let’s visualise that dense data into a bar chart.

The first conclusion I draw from the chart is that from 2010 to 2014 New Zealand Steel’s free allocation of emission units (the purple bars) materially exceeded their estimated liability to surrender units (the mid-pink bars) to match actual emissions.

The surplus units were not needed to compensate for increased energy costs caused by the NZETS as the NZETS did not cause any energy costs to increase. The free unit allocation was and is simply a transfer of wealth to New Zealand Steel in the form of a tradable right or voucher (the NZU emission unit) that is highly liquid.

The second conclusion is that although New Zealand Steel never needed to buy any extra emissions units to surrender under the NZETS, New Zealand Steel still owned about a million Emission Reduction Units at the end of both 2013 and 2014

So if New Zealand Steel always had more than enough free units to meet it’s obligation to surrender units under the NZETS, why would it also buy international units? There is only one plausible answer. It is to make an arbitrage profit.

Why am I so sure New Zealand Steel carried out arbitrage trades with its NZUs and surrendered cheap dubious ERUs rather than the free gifted NZUs for 2013 and 2014? It’s the maths.

Data from the Emissions Unit Register, NZEUR Holding & Transaction Summary, which I have summed into a Google sheet, tells us that for 2013 the total numbers of NZUs surrendered by all emitters was 732,667 and 576,470 NZUs were surrendered for 2014.

If New Zealand Steel had used its free NZUs to meet its 2013 unit surrender obligation, the number of NZUs would have to be roughly consistent with my estimate of half of it’s emissions or 873,750 units. All NZETS emitters collectively surrendered fewer units (732,667) for 2013! It is mathematically impossible for New Zealand Steel to have met those surrender obligations with NZUs. It must have used ERUs.

Here is a hypothetical example of what New Zealand Steel might have done.

According to a Carbon Forest Services webpage that tracks emission unit prices, on 11 October 2013, New Zealand units (NZUs) had a market price of $4.20 each and the Russian or Ukrainian Emission Reduction Units (ERUs) had a market price of 35 cents each. One NZU was worth 12 times as much as an ERU.

If New Zealand Steel had purchased 1 million ERUs on 11 October 2013 at 35 cents each or $350,000, it could then surrender 873,750 of them to the Government to match it’s 2013 emissions.

Based on that ‘if’, New Zealand Steel would then be in a position to sell all the 1,029,352 New Zealand units of the 2013 allocation at $4.20 each for a possible value of $4,323,278. The hypothetical profit would be $3,973,278.

Alternatively New Zealand Steel would keep the 1,029,352 NZUs and wait for their price to appreciate. In that case, the hypothetical but unrealised profit would be greater than $3,973,278.

That is just one possibility based on NZU and ERU prices on one date. I suggest you browse over to the Carbon Forest Services emission unit price chart and hover over it to see the differences between ERU and NZU prices from early 2013 to 2015.

Even when NZUs hit a historic low price of $1.60 in February 2013, they were still 9 times more valuable than ERUs. Choose your own combination of price difference and possible profit from buying ERUs and selling NZUs.

My final piece of evidence is Bluescope Steel Australia’s 2015 concise annual financial report which includes New Zealand Steel’s finances.

Note 6 Other Income says that in 2015 Carbon Permit income was $AUD 4.4 million. Footnote (a) says that the income is from the NZETS as the Australian Carbon Pricing scheme was abolished in July 2014.

Note 7 on page 63 says that ‘Direct carbon emission expense’ was a credit of $AUD 1 million.

Footnote (d) page 64 says that the current year carbon emission credit was due to the carbon ‘true-up’ of the Port Kembla steelworks.

So Bluescope Steel Australia made a carbon profit both sides of the Tasman! New Zealand Steel made $AUD 4.4 million out of the NZETS. So much for facing a carbon price at the margin!

Conclusion

New Zealand Steel really have achieved the ultimate emission trading scheme “two-fer”.

New Zealand Steel received a free allocation of emission units that is greater than the number needed to surrender for emissions. The availability of the cheaper imported Russian and Ukrainian international units highlighted by “Climate Cheats” gave New Zealand Steel the opportunity to make windfall arbitrage profits. New Zealand Steel did not pay a carbon price at the margin. New Zealand Steel probably made windfall arbitrage profits.

It seems that the more free units you give a company, the more it abuses the privilege of having an emissions trading scheme. “Climate Cheats” gives us an excellent history of the deeply unethical way the National-led Government has managed the New Zealand emissions trading scheme. The whole scheme is now so morally compromised it has no valid ethical basis to continue. Where I differ from the Morgan Foundation is what to do about it. They want to fix it. I think the NZ emissions trading scheme should be abandoned.

And this is why the NZ ETS has to go!

Aided and abetted by a compliant govt, major Polluters cheat and the Govt turns a blind eye.

“Bana Republic” is perhaps an apt label for the shenanigans that NZ governments have permitted, aided and constructed to aid our polluting businesses.

In the end, you can’t have the outcome (significant reductions in actual CO2 emissions), without actually reducing your emissions ! Kindergarten stuff really.

The Carbon Trading ideas would have some merit if everybody played by the rules. But in an international system where there are predominantly sharks in the water who’s aim is not to save humanity from its greedy self but to enrich themselves while the world “burns”, these systems simply do not seem to work and instead corrupt the minds of those who should know better in leading us through the extraordinary future we are “planning” for our descendants.

I think overall you are probably right that allocation has been a windfall to NZ Steel

But there are some things that your analysis seems to be missing. NZ Steel are the second largest consumer of electricity in NZ and the electricity market passthrough costs (not emissions) associated with this form part of the Govt’s compensation. This means that the windfall might not be as large as your analysis suggests (as their ETS costs depend on more than just their direct emissions).

This is further complicated by the fact that they could be exporting electricity during periods of low production and would gain a further windfall *if* the marginal generator has a higher emissions cost than NZ Steel’s generation because all generators receive the price asked by the marginal generator.

Regardless there was definitely a big arbitrage opportunity but this was also something that forestors exploited through re-registration arbitrage.

Troy,

Yes I skimmed fairly lightly over the issue of ‘NZETS energy/electricity market pass-through costs’. It is a very wonky issue to blog about.

It all depends what the NZETS ‘energy/electricity market passthrough costs’ to New Zealand Steel actually are. These costs must have declined if emissions units prices drop from dollars to multiples of ten cents. I think I am fairly safe in assuming they are insignificant if not zero to NZ Steel. Check these references.

Covec’s 2011 report ‘Impacts of the NZ ETS: Actual vs Expected Effects’ prepared for the 2011 ETS Review Panel could not find any increases in electricity, natural gas or coal prices caused by the NZETS.

Officials supporting the 2012 Finance and Expenditure Select Committee queried the five major electricity generating companies about NZETS costs flowing through into wholesale electricity prices. Their reply was; “costs being passed through directly from the NZETS are not visible or distinguishable due to the wholesale market pricing mechanism and these costs are not directly passed through due to competition factors”.

The New Zealand Emissions Trading Scheme evaluation report 2016 states on page 38;“The prices of emission units have been too low to affect business costs either for participants or those who receive costs passed down from participants”.